June Musings

Quick, raw thoughts

SpaceXAI. Elon has two classic playbooks: combining synergistic companies and driving down the cost of his products. He has executed the first with the creation of SpaceXAI, and I believe the second is in progress. In the case of Tesla, the acquisition of SolarCity rounded out his battery empire into a vertically integrated renewable energy company. The Roadster, his first electric car, was priced out of reach for most people. But Tesla's EV prices have come down progressively from the Model S to the Model 3. SpaceX is driving down the cost of launch by amortizing the rocket across several launches. The trade-off is the total payload that can be sent to space on each launch, but converting a large one-time capex into a smaller depreciation item has made space launch much more accessible. I expect to see something similar with xAI's datacenter play. Google is paying $7.78 per GPU per hour while Anthropic is paying $11.45. The bottleneck is driving the economics here. But as Elon executes on his chip play, he will drive down the all-in cost of building a datacenter. Silicon Data's latest round is being led by two of his closest allies, Antonio Gracias at Valor and Gavin Baker at Atreides. Pricing insight will be crucial to understanding the economics of compute. It's only a matter of time before his second act kicks in.

Futures market for compute. Ornn and Silicon Data are getting attention for their tie-ups with ICE and CME, both racing to build an index that accurately captures the price of GPU compute. From a utility standpoint, it's obvious. Hedging smooths a volatile price curve, which cuts credit risk, which drives down financing costs for compute producers. I've written about this before. The execution of Ornn and SD, though, is a bit different from what I would have imagined. If I were in their shoes, I'd put more effort into building an exchange myself. Polymarket and Kalshi are valuable as a result of the fees they are charging for each prediction. Same idea with Coinbase. Charging a transaction fee for compute could become just as valuable.

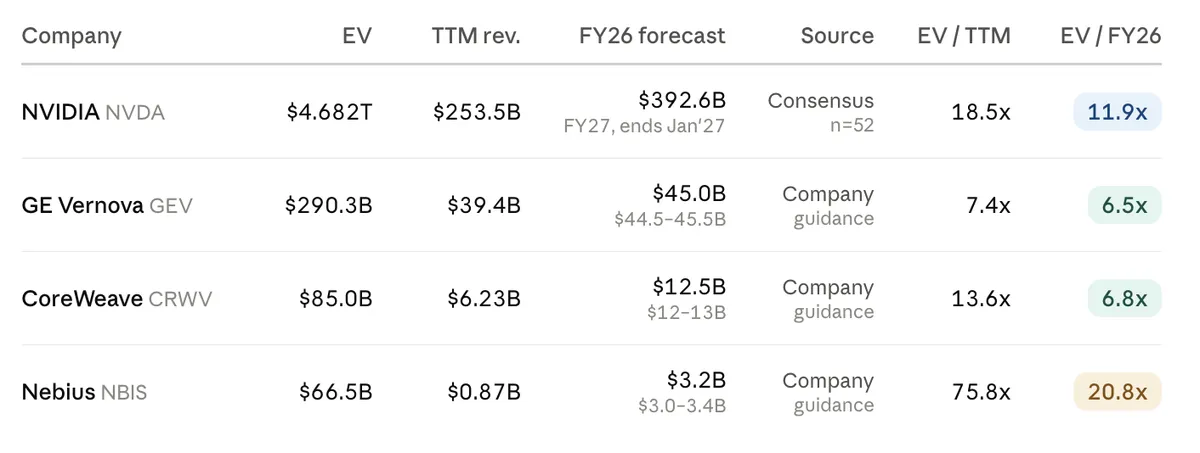

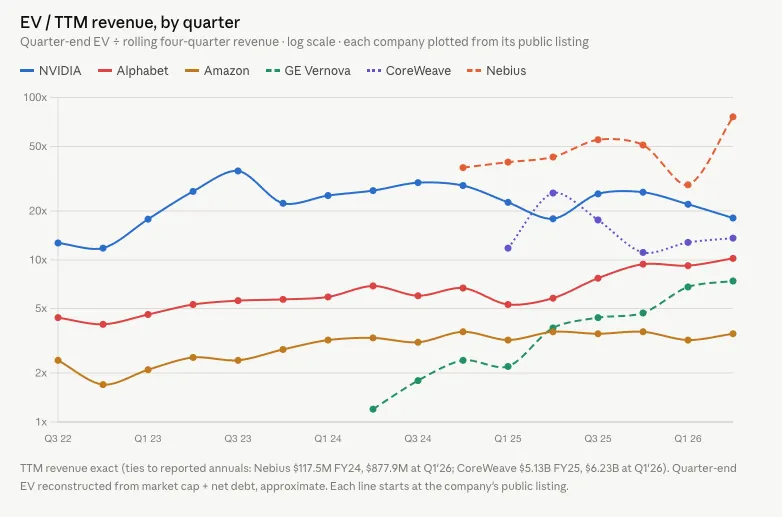

Will you buy into the compute or the stack? As David Einhorn said, reduce the basis risk by investing as directly in the thesis as possible. Once compute trades on a futures market, investors will be able to make more precise bets on compute. Across the universe of investable categories, the market is already favoring certain companies on a multiples basis (excuse the simplistic framing). Each company, in a way, is a form of leverage. A bet on increasing margin or sales, hopefully alongside multiple expansion to boost returns. The question for me is where that multiple will ultimately converge across the different categories of companies out there. An interesting exercise is to value these companies against a denominator that equalizes their contribution to the end product, something like a token. Then you can see how the market is valuing each one's contribution to the AI stack. A crude (and again, simplistic) version might use a metric like EV/Sales. It doesn't create a uniform denominator, since every dollar of revenue is the result of a different business activity, but it gives you a starting point. On that basis, the market is clearly valuing a dollar generated by Nebius extremely highly. Based on the multiples, either CoreWeave is significantly undervalued or Nebius is extremely overvalued.

Learnings from oil. Opaque pricing favors the compute providers. It lets them set their own prices, not unlike the Seven Sisters and the early days of OPEC when they used posted prices. Pricing can flex on a per-customer basis via rebates and discounts without fear of alienating everyone else. So from an adoption standpoint, compute providers will not want a futures market, since it implies pricing transparency (this assumes the successful execution with reliable data, which is also the biggest risk for data providers and exchanges looking to enter into this space). Still, the history of oil futures offers some useful lessons for the market now emerging. In oil, it was volatility in the form of supply and price shocks that led to the emergence of a futures market. Both buyers and sellers of crude and its products realized that they needed a way to hedge prices or lock in future supply. Price fluctuations also meant mispricing, and mispricing meant opportunities to make money, which got the interest of speculators. The market demand for an oil futures contract was there, just not clearly stated. NYMEX seized the moment, creating a liquid market by asking traders to participate, architecting an effective contract using WTI for delivery at Cushing via pipeline, and turning itself from a potato and platinum exchange into an energy powerhouse.